Posted on September 23, 2025

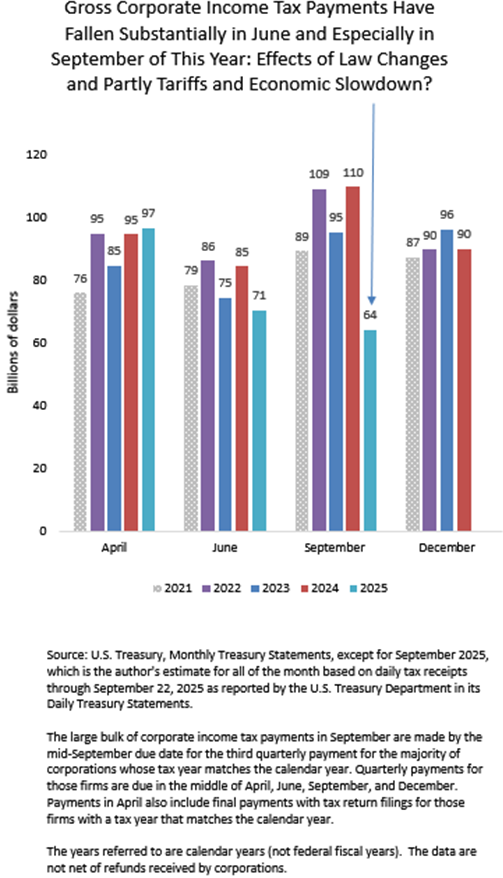

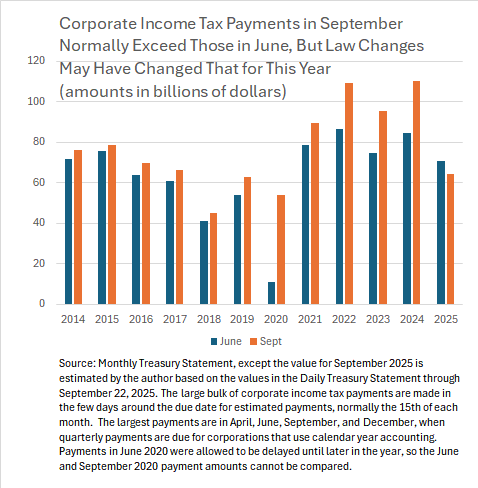

We have in the books the large bulk of corporations’ September payments of income taxes, the third quarterly payment for most corporations, and they show a big drop. We won’t be sure of the actual amount until all payments are in for September, but they look to be over 40 percent lower than the amount in September 2024, and even down some 10 percent or so compared to this year’s June payment, the one for the second quarter (see the first chart below). In a growing economy, the September payment normally exceeds the June payment and indeed had in the previous 10 years (see the second chart below). Payments in June were also weak, but not nearly as much as in September. All we observe is the payment amounts that arrive at the U.S. Treasury; it takes months or years to get data from corporate tax returns and other sources on the underlying incomes, deductions, and other factors generating the tax payments. For now, we are left to try to infer the causes based on what we do know.

The budget reconciliation legislation that was enacted into law in July is likely the biggest source of the large drop in corporate tax receipts. Among the many provisions, the legislation provided corporations with some new tax benefits that significantly affect fiscal year 2025 receipts: the most notable are faster deductions for equipment investment (so-called 100 percent bonus depreciation) and most domestic research and development costs–all effective for the current 2025 tax year (and even retroactive for some smaller firms’ R&D expenses). The Joint Committee on Taxation, the official Congressional estimator of the effects of tax law changes under consideration by the Congress, estimated that those two provisions reduce total federal revenues by about $87 billion in fiscal year 2025 (thus through September), and a big chunk of that is presumably a loss in corporate income tax receipts. It is difficult, though, to accurately estimate the immediate quarterly pattern of revenue effects from legislative changes.

The timing of the drop in corporate receipts suggests that more is at work than just the tax legislation. When firms make their quarterly payments, they estimate their profits for the full year and adjust their quarterly payments accordingly. If tax law changes, then firms also build that into their quarterly tax payments. The reconciliation legislation was enacted into law in early July, so corporations really shouldn’t have been assuming that it would be enacted when they made their mid-June payments–even though the legislation was winding its way through the Congress in June. Yet, corporate tax payments in June were down by about 16 percent compared to the amount paid in June 2024, while the April payment was comparable to the year-ago amounts.

The significant decline in corporate tax payments in June leads me to think that higher tariffs and some overall economic slowdown may also be playing a role. Revenue from tariffs has increased substantially in recent months (see post of August 27), starting mostly in April and continuing through the summer. To the degree that firms have absorbed the higher costs, rather than passing them along to customers in higher prices, means lower profits and tax payments. (Some of the tariff amounts could instead be absorbed by foreign-operating companies and lower their profits and thus affect neither U.S. prices nor U.S. corporate profits and tax payments, but that takes certain market conditions that are less common.) And a general economic slowdown often first shows in corporate profits, as firms delay cutting workers’ hours or their employment altogether unless the slowdown continues or worsens. Thus, there could be some component of general economic slowdown involved in the reduction in corporate tax payments starting in June, but it is difficult to know given the other effects from the tax legislation and tariffs.

Assessing corporate income tax payments when data on the underlying sources of the payments are months or years away is a challenge that those who do it for a living, trust me, know all too well.