Posted on April 2, 2026

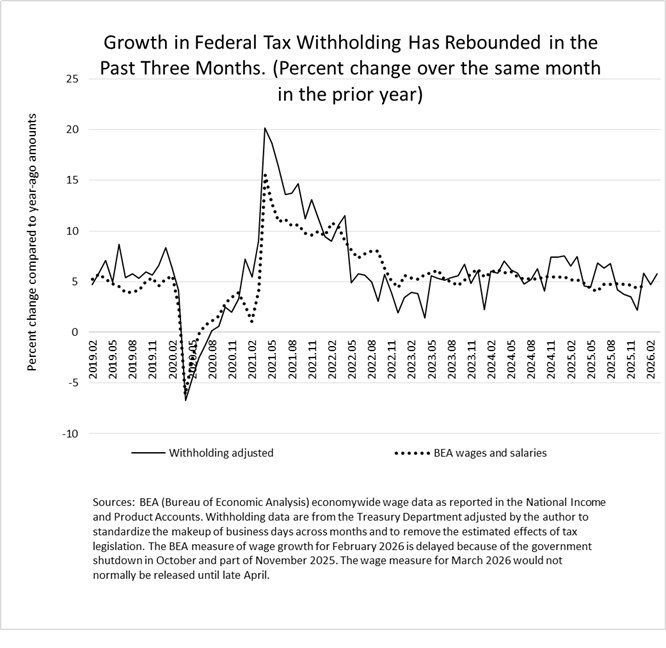

Now that the March data are in, we have observed three consecutive months of rebounding growth in federal tax withholding–which is the economywide amount of income and payroll taxes that employers withhold from workers’ paychecks and remit to the Treasury Department as soon as the day after the workers are paid. Specifically, we estimate that tax withholding grew by 5.7 percent in March compared to the amounts from March 2025. That follows growth rates of 4.7 percent in February and 5.8 percent in January, again compared to year ago amounts. Thus, on average, growth in the first quarter was about 5.4 percent, which is significantly higher than the 3.2 percent averaged in the fourth quarter of 2025.

Over extended periods of time, growth in tax withholding tends to move with overall wages and salaries in the economy (see the chart below). That is no surprise since a worker’s tax withholding is determined by the amount of their wages and salaries along with various other factors. Therefore, the pickup in withholding growth in the first quarter of 2026 suggests some pickup in wages and salaries.

We expect that significant growth in year-end bonuses in financial markets pushed up withholding growth at the beginning of the calendar year. But that doesn’t explain the strength in withholding in March, when the bonus season should be largely completed. It’s far too early for higher gasoline prices and inflation to feed through significantly to wages. Perhaps it is that we have just one month of data after the main bonus season, so we need to see if withholding continues to grow at its recent rate to make sure that the March results weren’t a short-term anomaly. If it was not an anomaly, then we may be seeing signs of an improving labor market.

For some greater detail (always your hint that this may be even deeper into the weeds), note that we adjust the withholding growth for estimated effects of tax law changes (see our methodology). That adjustment puts withholding growth on a constant law basis (that is, pre-law change basis) that should correspond more closely to economywide wage and salary movements. Until this year, we had gone over three years without needing to make adjustments to the withholding data for legislative effects (except for one month that was affected by some timing shifts). However, enactment of the 2025 Reconciliation Act (also known as the One Big Beautiful Bill) affects withholding starting around the beginning of this year, reducing it, according to our estimates, by roughly 0.6 percentage points. We add that relatively small effect to observed withholding growth in order to obtain a constant law measure. For example, in March, we observed withholding growth of about 5.1 percent (compared to year-ago amounts), but we estimate that it would have been 5.7 percent without the effects of the law changes. That is the amount we use to assess the health of the current labor market.