Posted on March 4, 2026

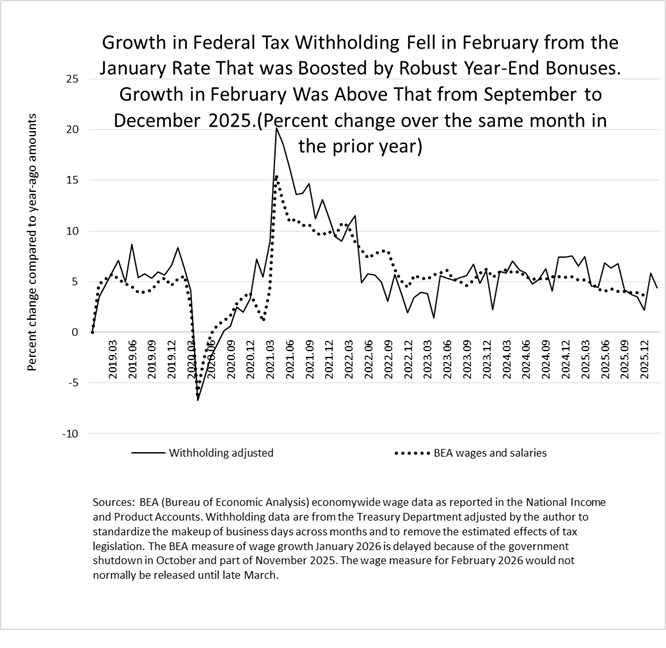

In February we observed growth of federal income and payroll tax withholding fall from the amount estimated for January, when we believe withholding was temporarily boosted by robust year-end bonuses on Wall Street. Nonetheless, withholding growth in February was a bit above the rates from September to December of last year (see the chart below). Because withholding measures the economywide amounts of income and payroll taxes withheld from workers’ paychecks by employers and remitted to the Treasury Department as soon as the day after the workers were paid, it correlates with overall wage and salary payments and the data are available on close to a real-time basis.

Specifically, we estimate that withholding grew by 4.4 percent in February compared to the amounts from February 2025 (so-called year-over-year growth). That growth was between the one-month jump in January (at 5.8 percent) and the growth from September to December 2025 (which averaged 3.4 percent). That growth late last year was consistent with wages and salaries in the overall economy that were growing just slightly faster than prices.

Note that some new federal tax law changes affecting tax withholding this year were enacted in the 2025 Reconciliation Act (also known as the One Big Beautiful Bill, but that name was stricken from the final legislation). We expect that the new provisions reduce withholding by relatively small amounts, on the order of 0.5 percent initially to maybe 0.8 percent as the year progresses. We base that estimate on several factors: the provision-by-provision revenue estimates by the Joint Committee on Taxation (Congress’s estimator of the revenue effects of tax provisions when under consideration); new withholding tables put out by the Treasury Department for 2026; the movements in withholding in the first part of this calendar year; and our analysis that shows workers are very slow to actively modify their withholding amounts, meaning that workers’ withholding is mainly affected by law changes that automatically and directly affect withholding through withholding table changes (like, in this case, the higher regular standard deduction and slightly expanded first two tax brackets).

We expect to shortly start building in those estimated legislative effects into our withholding estimates, because our goal is to estimate withholding growth on a constant law basis (thus removing the estimated effects of legislation). In that way, we obtain estimates of withholding growth that should better align with growth in wages and salaries in the economy.